Limo Insurance Coverage: 12 Powerful Tips Every Operator Must Know in 2025

TL;DR: Limo Insurance Coverage is the financial shield for your vehicles, passengers, drivers, and reputation. Cheap policies often hide exclusions that lead to denied claims. In high-risk markets like Houston, operators such as TransGates Limousine need higher limits, UM/UIM matching, and smart add-ons—while saving safely with telematics, clean MVRs, and right-sized deductibles.

Introduction

Limo Insurance Coverage isn’t just a line item—it’s the backbone of a sustainable limo business. Whether you run two vehicles or a 40-unit fleet, insurance typically ranks among your top three expenses. Focusing only on the monthly payment is risky; one uncovered loss can erase years of profit. In fast-moving hubs like Houston—with airport congestion, cruise-terminal surges, and high uninsured-driver rates—coverage is your survival plan. This guide gives you a practical framework to balance protection, contracts, and cost.

Why Limo Insurance Coverage Matters

A strong policy protects five pillars of your business:

- People: Passengers and drivers after injuries.

- Assets: High-value vehicles and equipment.

- Liability: Lawsuits and third-party damages.

- Reputation: Your brand and client trust.

- Contracts: Airport, hotel, and corporate requirements.

Under-insuring may save $150/month but can result in denied claims, low payouts, or lost accounts. Smart operators “buy coverage,” not payments.

Core Components of Limo Insurance Coverage

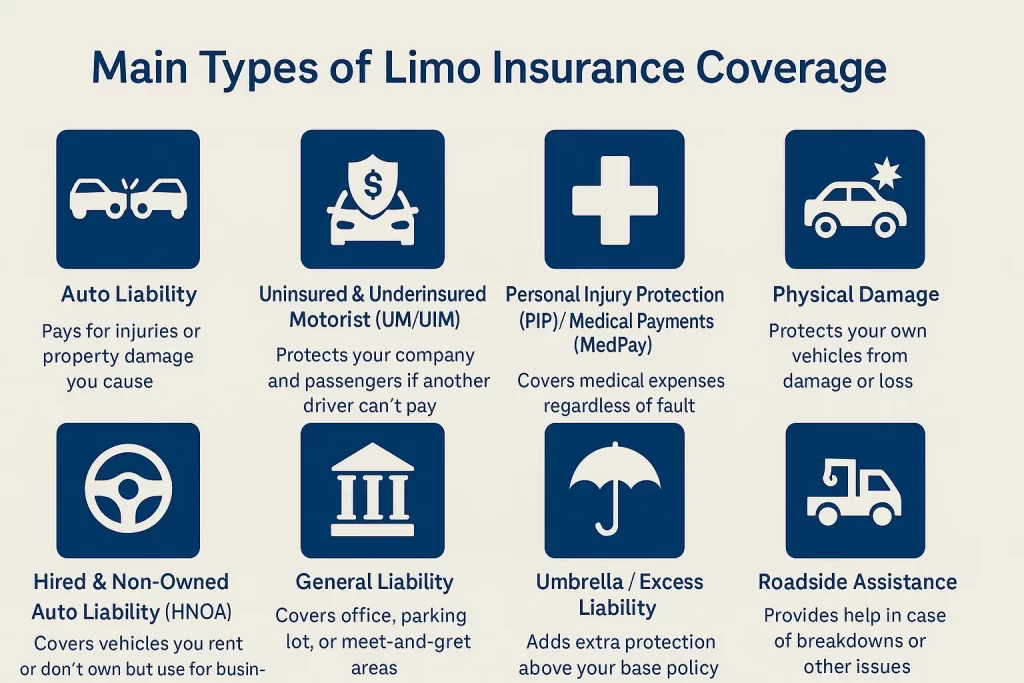

1) Auto Liability (Foundation)

Liability covers bodily injury and property damage you cause. Most contracts (airports, cruise lines, corporations) require $1,000,000 CSL. Larger fleets or VIP work may benefit from $1.5M–$2M. In Houston the City of Houston / ARA (Administration & Regulatory Affairs) require minimum of $500K liability, but is that enough to cover you?

2) Uninsured/Underinsured Motorist (UM/UIM)

When another driver can’t pay (common in large cities), UM/UIM pays for injuries to your passengers and drivers. Recommendation: match your liability limit, ideally $1M.

3) PIP / MedPay

Personal Injury Protection (PIP) or MedPay covers medical expenses regardless of fault. In Texas, the minimum is $2,500 per person, but many limo operators choose $5,000–$10,000 to reflect rising medical costs.

4) Physical Damage (Comp & Collision)

Protects against collision, theft, flood, hail, vandalism, and more. Insure newer or financed vehicles with a deductible of $2,500–$5,000. Use Stated Value to avoid low ACV payouts on specialty vehicles.

5) Hired & Non-Owned Auto (HNOA)

If you rent vehicles for seasonality/maintenance or subcontract to affiliates, HNOA is essential. Without it, your business could be exposed to third-party losses you don’t directly control.

6) General Liability (GL)

GL handles non-driving risks: slips at your office or staging lot, signage injuries, etc. Common limits: $1M per occurrence / $2M aggregate.

7) Umbrella / Excess Liability

Adds $1M–$3M above your other policies. Valuable for executive clients, larger fleets, and high-exposure markets like Houston.

Houston-Specific Considerations

- Higher collision exposure: Busy interchanges, toll roads, and airport loops (IAH/HOU).

- Uninsured drivers: Elevated rates make UM/UIM non-negotiable.

- Cruise traffic: Galveston terminals boost seasonal risk (pedestrians, luggage, buses).

- Contract demands: Hotels, FBOs, and corporations often require strict certificates.

Local leaders like TransGates Limousine pair strong limits with safety programs—telematics, dashcams, documented maintenance, and driver coaching—to manage loss frequency and premium trends.

Optional Coverages Worth Adding

- Roadside Assistance & Towing

- Rental Reimbursement (keep trips moving during repairs)

- Full Glass (windshields for SUVs/Sprinters add up)

- Garagekeepers Legal Liability (if you store client vehicles)

- Cyber/Data Liability (bookings, payments, PII)

- Employee Dishonesty (cash, fuel, electronics)

Cost-Saving Strategies (Without Risk)

- Dashcams & telematics: Many carriers offer 5–10% credits for verified safe driving.

- Clean MVRs: Audit driver records quarterly; remove high-risk drivers fast.

- Higher deductibles: $5,000 is common on high-value SUVs and Sprinters.

- Annual coverage review: Adjust to fleet age, valuation, and lender requirements.

- Liability-only on older units: Don’t over insure easily replaceable vehicles.

Case Study: The $42,000 Lesson

A Houston operator switched to a cheaper policy to save $220/month. After a total-loss collision, the insurer paid Actual Cash Value, not the true replacement cost. The operator lost two corporate accounts, missed 19 service days, and still had to fund a new vehicle. The combined hit—cash, downtime, and lost contracts—exceeded $42,000. Cheap insurance turned out to be the most expensive choice. For a deeper breakdown of the most common errors operators make with their coverage, review this guide on the top limousine insurance mistakes and how to avoid them.

Recommended Policy Checklist

- $1,000,000 Auto Liability CSL (or higher as required)

- UM/UIM limits matching Liability (ideally $1,000,000)

- PIP/MedPay at $5,000–$10,000

- Physical Damage with Stated Value and appropriate deductibles

- Hired & Non-Owned Auto (HNOA)

- General Liability $1M/$2M

- Umbrella/Excess $1M–$3M

- Telematics & dashcams for credits and loss control

- Written affiliate/subcontractor agreements

Pro Tips for Fleet Owners

- Bundle policies: Auto, GL, and Umbrella with one carrier where possible.

- Document safety: Quarterly safety meetings, driver coaching, and maintenance logs.

- Photograph vehicles monthly: Exterior/interior condition aids claims and resale.

- Choose livery-savvy agents: Familiar with Texas and large-market (Houston) risks.

- Position your brand: Like TransGates Limousine, communicate safety standards in proposals.

Internal & External Resources

FAQs

What is the minimum Limo Insurance Coverage I need?

Most contracts require $1,000,000 CSL liability. Some corporate and public-sector accounts mandate higher limits. Always verify certificate requirements before bidding.

Should UM/UIM match my liability limit?

Yes—especially in large markets like Houston where uninsured drivers are more common. Matching limits (e.g., $1M) protects passengers and drivers when the at-fault party cannot pay.

Is increasing PIP from the state minimum worth it?

Typically, yes. Medical costs are rising, and $5,000–$10,000 PIP helps manage short-term expenses and reduces downtime for drivers and passengers after incidents.

How can I lower premiums without weakening coverage?

Use dashcams/telematics for 5–10% credits, raise deductibles strategically, maintain clean MVRs, and conduct annual policy reviews. Apply liability-only to older units that are inexpensive to replace.

Conclusion

Limo Insurance Coverage is the foundation of a resilient limousine company. The smartest operators don’t chase the cheapest payment; they engineer the right mix of limits, UM/UIM, PIP, Physical Damage, HNOA, GL, and Umbrella—then reduce total cost with safety tech and disciplined driver management. That’s how brands like TransGates Limousine protect passengers, win contracts, and grow sustainably in competitive markets like Houston.

If you’re a limousine operator in Texas, you don’t have to navigate the complex world of insurance alone. The Houston Limousine Association empowers local operators with expert insights, group discounts, and professional guidance to help you secure the best limousine commercial auto insurance coverage at the most competitive rates. Protect your investment, strengthen your business, and connect with trusted industry leaders — get a membership plan today and drive your success forward with confidence.

{kind=link}